TOPIC 8: ACCOUNTS ~ MATHEMATICS FORM 3

TOPIC 8: ACCOUNTS ~ MATHEMATICS FORM 3

ACCOUNTS

Double Entry

The Meaning of Double Entry

Explain the meaning of double entry

The process of keeping record is called bookkeeping. The simplest form of bookkeeping is single entry.

ACCOUNTS

Every transaction is recorded once. This is unreliable because:

If an arithmetic mistake is made, it is very difficult to find and correct it

If a transaction is omitted, it is difficult to find it

The sales ledger

The purchases ledger

The general ledger

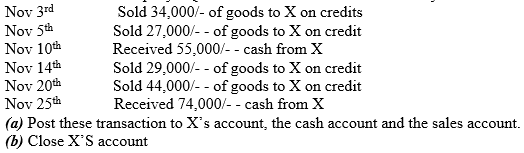

is a person who owes money to the business, that is a person to whom the business sold goods on credit.

ACCOUNTS

So when the business has a new customer, it will open an account in the sales ledger for that customer.

supplier.

Is a ledger that records all accounts other than debtors’ and

creditors’ accountants.

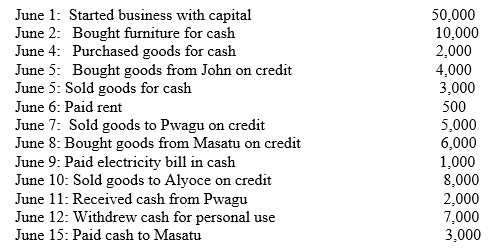

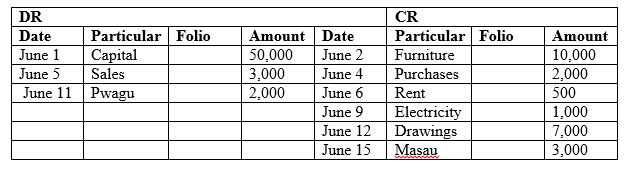

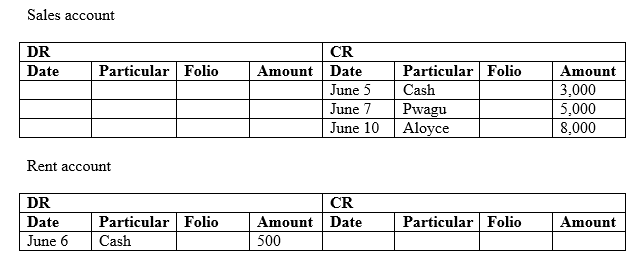

-Double entry: Is a bookkeeping system whereby every transaction is recorded twice in the ledger.

ACCOUNTS

It is recorded on the left as debit (DR), and on the right as credit (CR).

The bank account gives the benefit, and so is credited 50,000/-

The wages account receives the benefit, and so is debited 50,000/-

ABC Limited has given the benefit, and so is credited 100,000/-

The fixed assets account has received the benefit, and so is debited 100,000/-

ACCOUNTS

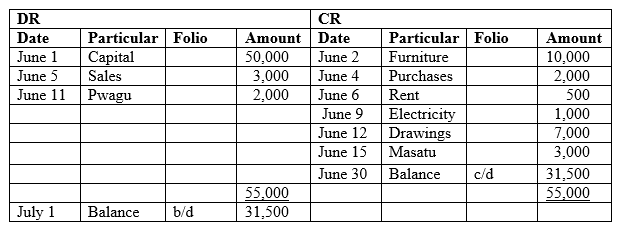

Example 1

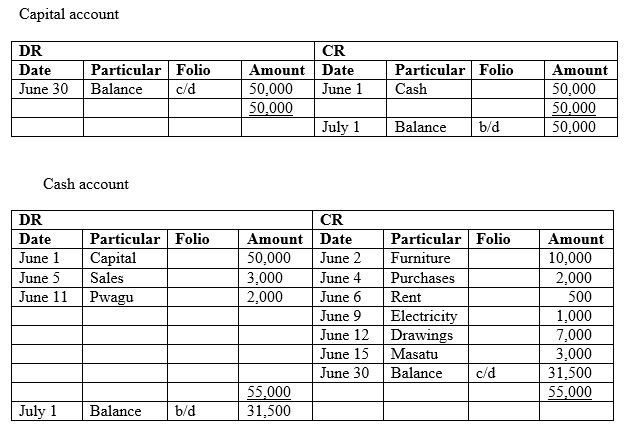

Hence the capital account is credited and he cash account is debited.

ACCOUNTS

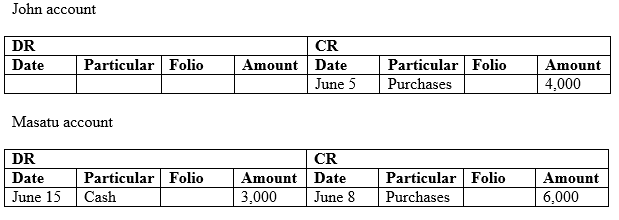

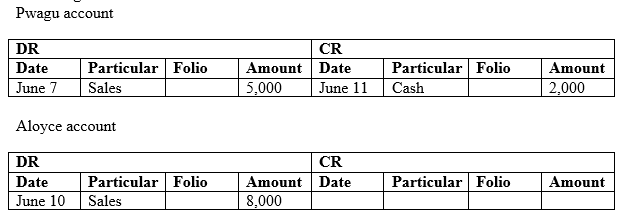

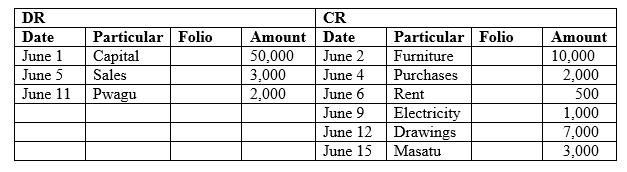

In the’ Particular’ column, write the other account involved in the transaction.

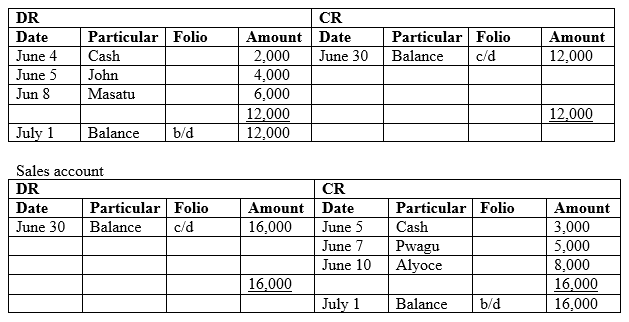

purchases ledger.

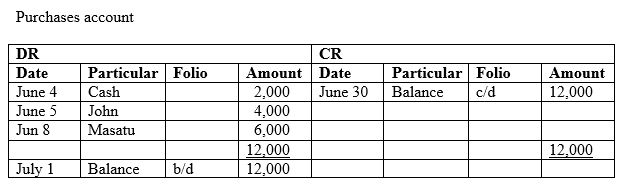

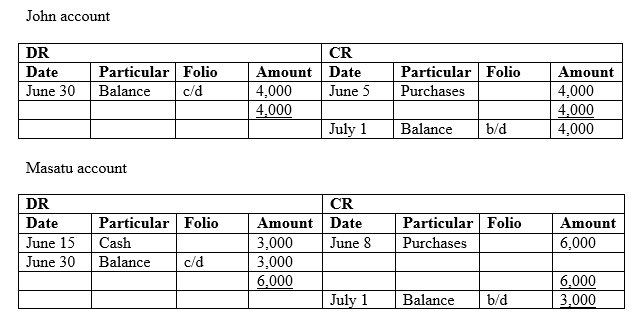

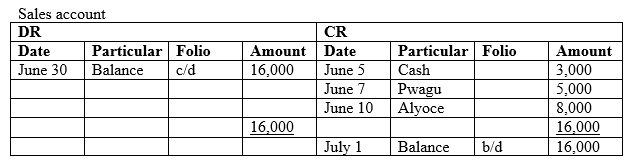

ACCOUNTS

ACCOUNTS

PURCHASES LEDGER

ACCOUNTS

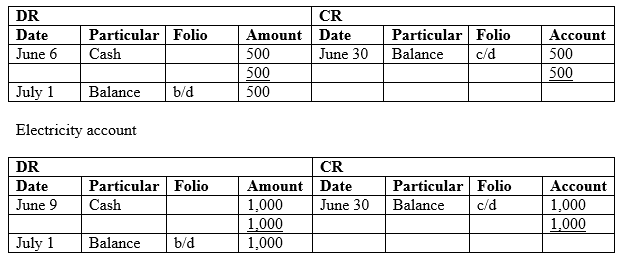

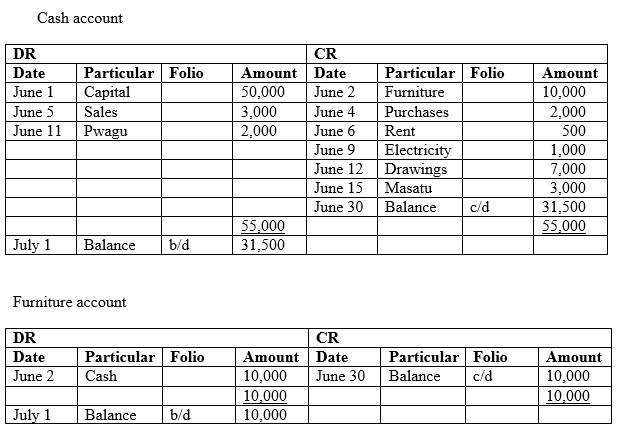

Note: Check that for each transaction there are two equal entries, one for debit and one for credit, for instance:

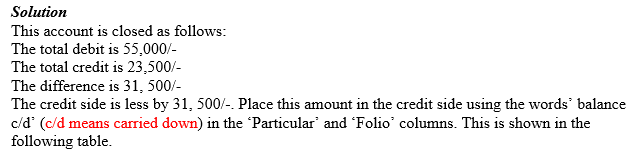

the accounts is the process of balancing the accounts. This involves

determining the totals of the debits and credits, and finding the

difference between the two sides. The difference is the balancing figure, which is placed in the side that is less. This makes the two sides equal.

balance c/d shows the amount that stands on the account on the closing

date. It appears as balance b/d (b/d means brought down) on the opening

date of the next trading period, on the other side of the ledger.

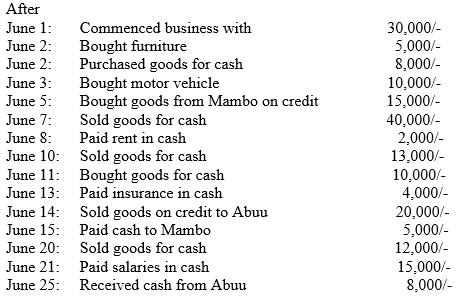

- a lorry bought for cash

- goods sold to Mr. Sabaya for cash

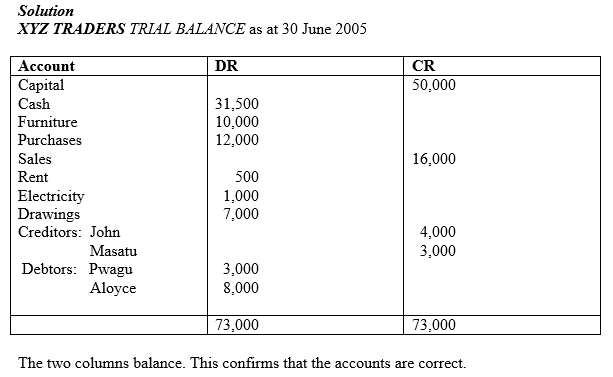

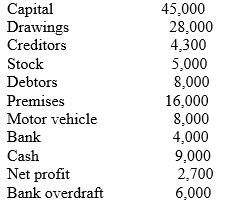

is a statement which shows the balances of accounts extracted from the

ledger. At the end of each trading period, the accounts in the ledger

are closed, that is the balance of each account is determined. These

balances are then shown in the trial balance.

checks the arithmetical accuracy of the ledger. The double entry system

requires posting equal amounts to debits and credits. Therefore the

trial balance is expected to balance if the arithmetic was correct. If

there is a difference in the totals of the debit and credit columns of

the trial balance, then some errors were made.

simplifies the preparation of the final accounts. The trial balance

contains all the accounts extracted from the ledgers. This makes it easy

to post the accounts to the final accounts.

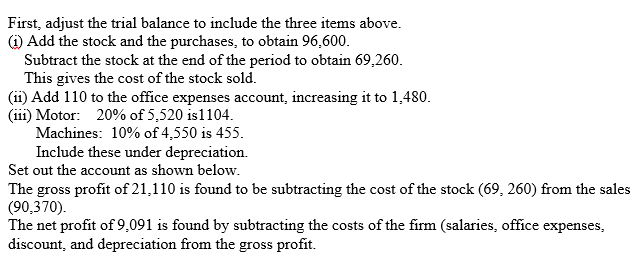

trading and profit and loss A/C is an account that is composed of two

accounts, the trading A/C, and the profit and loss A/C.

the profit and loss A/C, the gross profit and other revenues are

credited to the account while the operating expenses are debited.

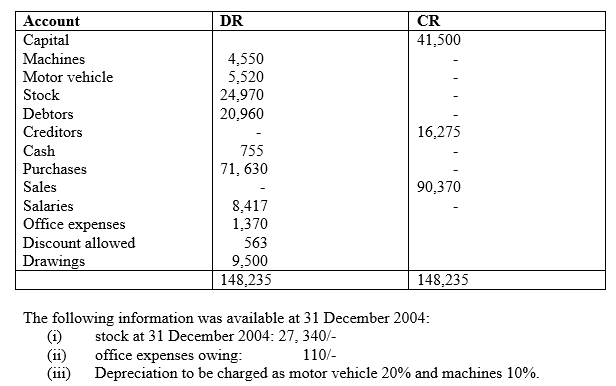

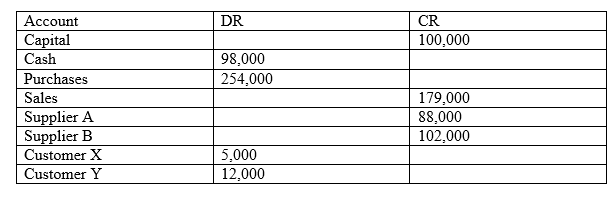

following is the trial balance of FMHN Trading Co. as at 31 December

2004. Prepare the trading and profit and loss accounts for the year

2004.

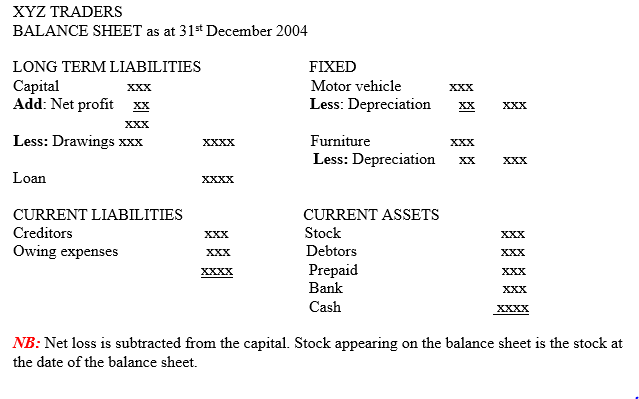

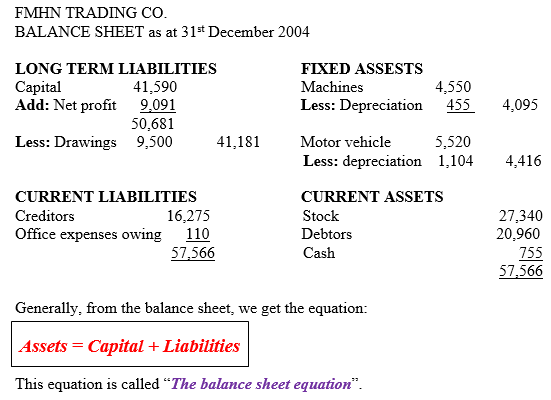

are possessions of the business that assist the business in its

operations, and benefit the business for more than one accounting

period.

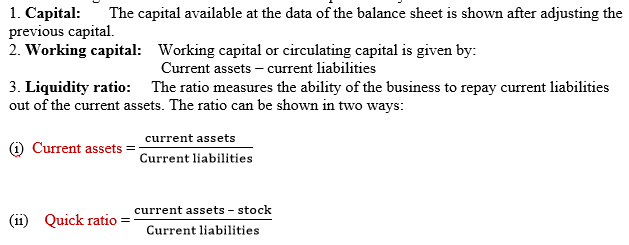

the balance sheet, useful information concerning the business can be

extracted. The interpretation then depends on the use of the

information.

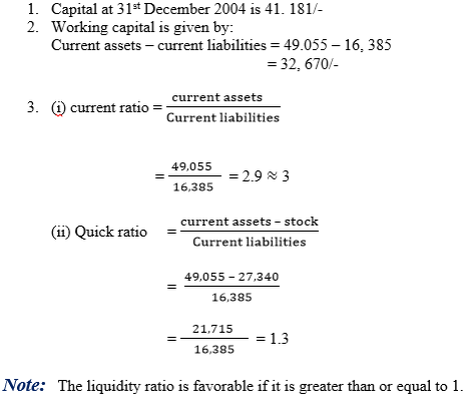

quick ratio measures the ability of the business to pay current

liabilities out of current assets excluding stock which is considered

less liquid.

- Working capital

- Quick ratio

- Current ratio

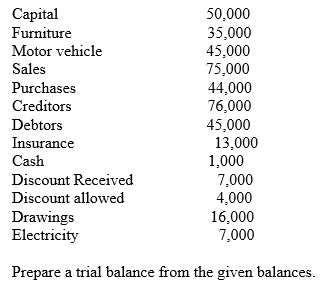

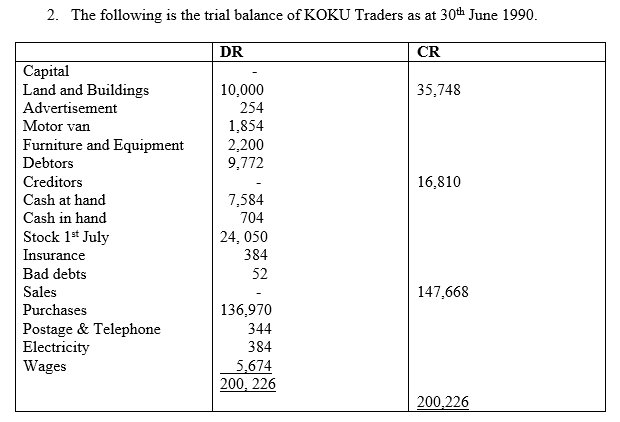

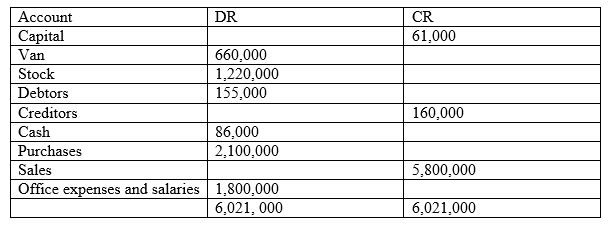

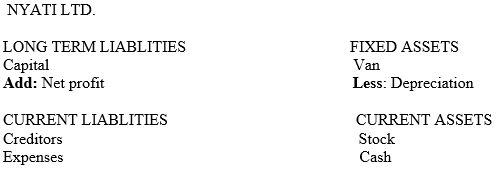

Below is a trial balance for Nyati Ltd. The closing stock was 1,

750,000/-, and the van was depreciated at 25%. Set up the trading and

profit and loss account.

- capital

- working capital

- current liquidity

- quick liquidity rate

I am actually glad to glance at this blog posts which consists of lots of useful facts, thanks for providing these data.

0mniartist asmr

I think this is one of the most vital info for me.

And i’m glad reading your article. But should remark on few normal issues, The site taste

is great, the articles is truly great : D. Excellent process,

cheers 0mniartist asmr

This paragraph is genuinely a pleasant one it helps new the

web people, who are wishing in favor of blogging.

0mniartist asmr

I enjoy looking through an article that can make men and women think.

Also, many thanks for allowing for me to comment! asmr 0mniartist

This website was… how do I say it? Relevant!! Finally I’ve found something

which helped me. Thank you! 0mniartist asmr

Hello there I am so thrilled I found your site, I really found you by accident, while I was researching on Google for something else, Anyways I am here now and would just like to say thank you for a fantastic

post and a all round entertaining blog (I also love the theme/design),

I don’t have time to read through it all at the minute

but I have saved it and also included your RSS feeds, so when I have time

I will be back to read more, Please do keep up the excellent work.

0mniartist asmr

Hmm it seems like your blog ate my first comment (it was extremely long) so I guess

I’ll just sum it up what I submitted and say, I’m thoroughly enjoying your blog.

I as well am an aspiring blog blogger but I’m still new to the whole thing.

Do you have any tips for inexperienced blog writers? I’d certainly appreciate it.

0mniartist asmr

I’m not sure exactly why but this blog is loading very slow

for me. Is anyone else having this issue or is it a problem on my end?

I’ll check back later on and see if the problem still exists.

0mniartist asmr

I like the helpful information you provide in your articles.

I will bookmark your weblog and check again here regularly.

I am quite certain I’ll learn many new stuff

right here! Best of luck for the next! 0mniartist asmr

What’s up to all, how is everything, I think every one is getting more from this website, and your views are nice

designed for new people. asmr 0mniartist